Few movies capture the cold calculus of financial survival as precisely as Margin Call (2011). Set in the crucible of the 2008 crisis, it remains one of the most accurate and sobering films about Wall Street ever made.

Synopsis

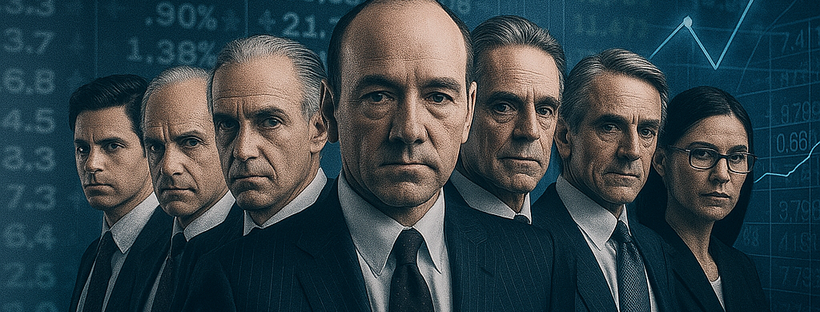

Set over 24 hours at a fictional Wall Street investment bank on the cusp of the 2008 crisis, Margin Call follows a chain of discovery that begins with a junior risk analyst (Penn Badgley) and a recently laid-off risk manager (Stanley Tucci) handing a USB drive to a young quant, Peter Sullivan (Zachary Quinto). Sullivan quickly models the firm’s mortgage portfolio and realizes the unthinkable: the bank is levered to the point that a modest move in credit spreads will wipe out its equity. Senior management—desk head Will Emerson (Paul Bettany), division chief Sam Rogers (Kevin Spacey), risk chief Sarah Robertson (Demi Moore), and CEO John Tuld (Jeremy Irons)—is summoned through the night.

By dawn, the decision is made. The firm will dump its toxic book at the market open, selling knowingly mispriced assets to counterparties before the street understands what’s happening. Traders are promised bonuses to “be first out the door,” reputations be damned. The firm survives, but at the cost of its trading relationships and moral compass. The spoiler is the point: Margin Call is a procedural about decision-making under existential risk—what it means to choose survival when the price is trust, ethics, and the future franchise.

Cinematic Qualities

J.C. Chandor’s debut is restrained, almost theatrical. Most of the film takes place in conference rooms and trading floors after hours, which concentrates attention on dialogue and body language. The direction is confident: long, quiet takes allow the audience to do the math alongside the characters. The pacing is deliberate but never inert; each escalation—analyst to desk head to division chief to CEO—adds pressure, widening the decision horizon from a spreadsheet to a firm-wide triage.

The performances are uniformly strong. Spacey grounds the film, giving Sam Rogers the weary pragmatism of a manager who has buried more than one dog. Irons plays Tuld as the embodiment of late-cycle bravado—charming, ruthless, and untroubled by nuance. Tucci’s monologue about building a bridge years earlier lends a rare, human counterweight—reminding us that finance once financed something. Production design is spare and credible: phones, whiteboards, a Bloomberg glow. There are no flashy montages or trading clichés; the visual grammar respects how real decisions look—tired faces, stale coffee, and blinking P&Ls.

If there’s a shortcoming, it’s that the film’s austerity can feel hermetic; we barely see the market or the external world that will eat these trades. But the choice serves the theme: the catastrophe is internal long before it becomes public.

Trader’s Lens

Central Concepts

Leverage and tail risk. The bank’s Value-at-Risk (VaR) and stress models break under fat-tail dynamics; a small shift in assumptions reveals catastrophic exposure. The lesson is not that models are useless, but that leveraged balance sheets are intolerant of model error.

Liquidity risk. The firm’s assets are “liquid” until they aren’t. Tuld’s mandate—sell it all, now—weaponizes first-mover advantage but acknowledges that market depth collapses when everyone heads for the same exit.

Moral hazard and asymmetric payoffs. The bonuses for executing the fire sale illustrate incentives that reward short-term survival while socializing long-term costs to counterparties and, ultimately, the system.

Governance under stress. Decision rights migrate upward in a crisis. The film accurately shows how boards become spectators while concentrated authority (CEO + a small inner cabinet) acts with incomplete information.

Lessons for Traders

- Know your true distribution. The fatal error is mistaking historical volatility for risk. When correlation goes to one, the past is a poor map. Stress-test nonlinearly; include “break the bank” scenarios and act on them before they become your base case.

- Liquidity is a position. You trade your ability to trade. Don’t size a book to normal volumes; size to crisis volumes. Build funding redundancies. Run liquidity drills the way airlines run safety checks.

- First loss, best loss. The film’s cold logic—sell before the market knows—captures a hard truth: sometimes the optimal trade is reputationally ugly. The nuanced lesson: if every P&L depends on being first out, your strategy was fragile from the start.

- Incentives write the ending. Emerson’s desk sells because they are paid to. Align comp with risk horizons; clawbacks and deferrals are not moral niceties—they’re control systems.

- Communication is a risk tool. The meetings are crisp: who decides, what’s the exposure, what’s the plan? In a drawdown, ambiguity kills faster than bad news. Establish protocols before you need them.

Accuracy vs. Dramatization

Accurate:

- The technical trigger—a model that underestimates tail risk—is plausible. Banks in 2007–08 learned that small calibration errors explode under leverage.

- The politics are real: risk wants to be heard earlier; trading dismisses alarms as “model drift” until the CFO/CEO cares.

- The “dump day” playbook exists. Firms do liquidations under secrecy with sales credits dangled to ensure execution.

Dramatized/Compressed:

- The timeline is sped up. In reality, discovering, validating, escalating, and executing a firm-wide liquidation would take longer and involve more compliance, legal, and board minutes—even at 2 a.m.

- Counterparty reaction is off-screen. In practice, word leaks faster; axes move; spreads gap before the open. Some counterparties would fade prices immediately.

- Risk metrics are simplified for film. No one says “VaR” or “copula,” and that’s fine. The spirit is faithful: the map failed the terrain.

Psychology & Culture

Margin Call is less about villains than systems. The culture is a hierarchy of justified compromises. Sam Rogers loves his traders like a coach loves a team, yet he’ll hand them a script to sell radioactive paper to friends. Tuld is not a cartoon; he is capitalism’s amoral survival instinct, fluent in cycles: “There are three ways to make a living in this business…”—a pithy credo for exploiting spreads while they exist and walking away when they don’t.

The film captures the triad that governs market behavior:

- Fear: The stomach-drop when a model flips regime.

- Greed: The bonus carrot for pushing product you wouldn’t hold.

- Career risk: No one wants to be the first to call panic—or the last to act.

Ethically, the movie is pointed without preaching. It shows a firm that will sell toxic assets with full knowledge of their toxicity. Traders rationalize: “If we don’t, we’re dead.” That mindset pervades late-cycle markets: time horizons compress, empathy shrinks, and the focus narrows to the next print. The most haunting scene isn’t the liquidation; it’s Sam burying his dog at dawn—a quiet elegy for loyalty in a business that valorizes exit.

Audience Fit

- Retail traders: Valuable for understanding how liquidity, leverage, and incentives shape the tape you see. It won’t teach setups, but it will teach context.

- Finance students: A case study in governance, model risk, and crisis communication—arguably more instructive than a semester of textbooks if discussed critically.

- Industry insiders: Familiar terrain, but the film’s fidelity to tone and tempo makes it a mirror worth revisiting—especially for risk managers and COOs.

- General audiences: Accessible if you’re comfortable with boardroom dramas. The jargon is minimal; the stakes are clear.

Where It Teaches Best

Pre-mortems and tabletop exercises. Watch the film with your team and pause at each escalation: What would you do with partial information? Who owns the call to de-risk? What are your pre-set triggers? Which relationships would you sacrifice to save the firm? Replace the mortgage book with your biggest correlated bet—AI equities, crypto, rates—and the questions hold.

Comp design and culture. Use it to interrogate your own incentive scheme. If you needed traders to sell a poisoned book tomorrow, how would you get it done? If the answer is “offer a one-day windfall,” your steady-state comp may already be misaligned.

Risk reporting. The movie implicitly argues for two dashboards: the one you show every day and the one you hope you never have to open—the “kill-switch” view with liquidity haircuts, wrong-way risk, and stress to regulatory capital.

Shortcomings

The narrative flirts with fatalism. By presenting liquidation as the only rational move, it risks normalizing a narrow moral calculus. In reality, options exist: hedging residual risk, negotiating block trades with full disclosure to key counterparties, or seeking emergency funding—even if those paths are messy, dilutive, and career-threatening. The absence of regulators is also a gap; after-hours or not, a systemic unwind of this scale would intersect with supervisory eyes quickly. Yet the omissions don’t ruin the film’s core achievement: a credible portrait of decision-making at the cliff’s edge.

Verdict / Rating

9 / 10.

Trader’s takeaway: Margin Call is less about numbers than the psychology of survival in a collapsing system—an unflinching tutorial in how leverage, liquidity, and incentives converge in crisis. It teaches that the most dangerous risk is the one your culture learns to ignore, and that the worst day to discover your true distribution is the day you must trade it.

Bottom line: As cinema, it’s austere and riveting. As a trading case study, it’s essential viewing—particularly if you hold a book whose liquidity you’ve only ever tested on sunny days.